Newmont delivers solid second quarter production and free cash flow results from leading portfolio of long-life, responsibly managed assets; updates full-year guidance

DENVER–(BUSINESS WIRE)– Newmont Corporation (NYSE: NEM, TSX: NGT) (Newmont or the Company) today announced second quarter 2022 results.

SECOND QUARTER 2022 RESULTS

- Produced 1.5 million attributable ounces of gold and 330 thousand attributable gold equivalent ounces (GEO) from co-products, an increase of more than 130 thousand total gold equivalent ounces from the first quarter

- Generated $1.0 billion of cash from continuing operations and $514 million of Free Cash Flow (97 percent attributable to Newmont)*

- Reported gold Costs Applicable to Sales (CAS)* of $932 per ounce and All-In Sustaining Costs (AISC)* of $1,199 per ounce

- Adjusted Net Income (ANI) of $0.46 per share and Adjusted EBITDA of $1,149, impacted by increasing costs and declining metal prices

- Updated full-year guidance of 6.0 million ounces of attributable gold production, CAS of $900 per ounce and AISC of $1,150 per ounce; reaffirmed original guidance of 1.3 million gold equivalent ounces from copper, silver, lead and zinc with updated co-product cost guidance of $750 per GEO of CAS and $1,050 per GEO of AISC**

- Updated full-year guidance for development capital spend to $1.1 billion; Provided trends on development capital costs and timeline related to Tanami Expansion 2 and Ahafo North

- Declared second quarter dividend of $0.55 per share, consistent with the previous seven quarters***

- $1 billion share repurchase program to be used opportunistically in 2022, with $475 million remaining***

- Ended the quarter with $4.3 billion of consolidated cash and $7.3 billion of liquidity with a net debt to adjusted EBITDA ratio of 0.3x*

- Advancing profitable near-term projects, including Tanami Expansion 2, Ahafo North and Yanacocha Sulfides

- Completed acquisition of Sumitomo Corporation’s 5 percent interest in Yanacocha, increasing ownership in Sulfides project to 100 percent

- Maintained a clear focus on managing the critical controls that must be in place at all times to prevent fatalities; 155 thousand critical control verifications completed by leaders in the field

- Published our 2021 Sustainability Reporting Suite, including our second Annual Climate Report, prepared in accordance with the Task Force for Climate Disclosure (TCFD) framework, detailing the pathway to achieve 2030 carbon emissions reduction targets and 2050 goal

“Newmont delivered a solid second quarter performance, producing 1.5 million gold ounces and generating $514 million in free cash flow. Through our industry-leading portfolio of assets and projects, our proven integrated operating model, our balanced and disciplined approach to capital allocation and our values-driven commitment to our purpose of creating value and improving lives through sustainable and responsible mining, Newmont remains well-positioned to safely manage through the evolving and unprecedented challenges that face our industry and the world at large.”

– Tom Palmer, Newmont President and Chief Executive Officer

* Non-GAAP metrics; see reconciliations at the end of this release.

**See discussion of outlook and cautionary statement at end of release regarding forward-looking statements.

***See cautionary statement at the end of this release, including with respect to future dividends and share buybacks.

SECOND QUARTER 2022 FINANCIAL AND PRODUCTION SUMMARY

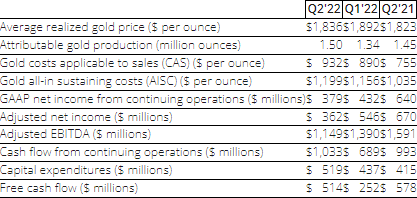

Attributable gold production1 increased 3 percent to 1,495 thousand ounces from the prior year quarter primarily due to higher ore grade milled at Boddington, Ahafo and Tanami and a draw-down of in-circuit inventory compared to a build in the prior year. In addition, the current quarter benefited from the increased ownership at Yanacocha due to the acquisition of Buenaventura’s 43.65% ownership in February 2022. These increases were partially offset by lower ore grade milled and lower throughput at Peñasquito and Éléonore.

Gold CAS totaled $1.4 billion for the quarter. Gold CAS per ounce2 increased 23 percent to $932 per ounce from the prior year quarter primarily due to higher direct operating costs as a result of inflationary pressures, driven by higher labor costs and an increase in commodity inputs, including higher fuel and energy costs; as well as lower by-product credits at Yanacocha and a draw-down of higher cost in-circuit inventory compared to a build in the prior year. In addition, Gold CAS includes the allocation of $22 million for the Peñasquito profit-sharing agreement entered into during the second quarter of 2022 related to 2021 results.

Gold AISC per ounce3 increased 16 percent to $1,199 per ounce from the prior year quarter primarily due to higher CAS per ounce.

Attributable gold equivalent ounce (GEO) production from other metals increased 9 percent to 330 thousand ounces primarily due to higher ore grade milled at Boddington and higher mill recovery and throughput at Peñasquito.

CAS from other metals totaled $327 million for the quarter. CAS per GEO2 increased 56 percent to $983 per ounce from the prior year quarter primarily due to higher allocation of costs to other metals and higher direct operating costs as a result of inflationary pressures, driven by higher labor costs and an increase in commodity inputs, including higher fuel and energy costs. In addition, CAS from other metals includes the allocation of $48 million related to the Peñasquito profit-sharing agreement entered into during the second quarter of 2022 related to 2021 results.

AISC per GEO3 increased 45 percent to $1,286 per ounce primarily due to higher CAS per GEO and higher treatment and refining costs.

Average realized price for gold was $1,836, an increase of $13 per ounce over the prior year quarter. Average realized gold price includes $1,858 per ounce of gross price received, an unfavorable impact of $14 per ounce mark-to-market on provisionally-priced sales and reductions of $8 per ounce for treatment and refining charges.

Revenue remained flat at $3.1 billion compared to the prior year quarter as higher average realized gold prices and higher gold sales volumes were offset by lower average realized co-product metal prices.

Net income from continuing operations attributable to Newmont stockholders was $379 million or $0.48 per diluted share, a decrease of $261 million from the prior year quarter primarily due to higher CAS predominately resulting from the impacts of inflation and the Peñasquito profit-sharing agreement entered into during the second quarter of 2022, as well as unrealized losses on marketable and other equity securities. These decreases were partially offset by lower income tax expense.

Adjusted net income4was $362 million or $0.46 per diluted share,compared to $670 million or $0.83 per diluted share in the prior year quarter. Primary adjustments to second quarter net income include changes in the fair value of investments and valuation allowance and other tax adjustments, including an $125 million tax settlement in Mexico.

Adjusted EBITDA5 decreased 28 percent to $1.1 billion for the quarter, compared to $1.6 billion for the prior year quarter.

Capital expenditures6 increased 25 percent from the prior year quarter to $519 million primarily due to higher development capital spend. Development capital expenditures in 2022 primarily include advancing Tanami Expansion 2, Yanacocha Sulfides, Ahafo North, Pamour and Cerro Negro District Expansion 1.

Consolidated operating cash flow from continuing operations increased 4 percent from the prior year quarter to $1.0 billion primarily due to a decrease in accounts receivable and increase in accounts payable due to the timing of receipts and payments to vendors, respectively, and a decrease in tax payments. These increases were partially offset by an increase in payments for reclamation and remediation obligations. Free Cash Flow7decreased to $514 million from $578 million in the prior year quarter primarily due to higher development capital expenditures, partially offset by higher operating cash flow.

Balance sheet and liquidity ended the quarter with $4.3 billion of consolidated cash and approximately $7.3 billion of liquidity; reported net debt to adjusted EBITDA of 0.3x8.

Nevada Gold Mines (NGM) attributable gold production was 290 thousand ounces, with CAS of $1,035 per ounce and AISC of $1,263 per ounce for the second quarter. NGM EBITDA9 was $218 million.

Pueblo Viejo (PV) attributable gold production was 70 thousand ounces for the quarter. Cash distributions received for the Company’s equity method investment in Pueblo Viejo totaled $48 million in the second quarter.

SECOND QUARTER 2022 EARNINGS DRIVERS

Compared to the first quarter of 2022, earnings were negatively impacted by higher labor, materials and consumables costs of approximately $80 million, higher fuel and energy costs of approximately $50 million and the $70 million expense recognized in the second quarter related to the Peñasquito profit-sharing agreement announced in early July. In addition, lower realized metals prices, including unfavorable mark-to-market adjustments on provisionally-priced sales, impacted earnings by approximately $225 million compared to the first quarter. These impacts were partially offset by approximately $250 million of higher sales volumes in the second quarter.

COVID UPDATE

Newmont continues to maintain wide-ranging protective measures for its workforce and neighboring communities, including screening, physical distancing, deep cleaning and avoiding exposure for at-risk individuals. The Company incurred incremental Covid specific costs of $10 million during the quarter for activities such as additional health and safety procedures, increased transportation and distributions from the Newmont Global Community Support Fund. The majority of the additional incremental Covid specific costs have not been adjusted from our non-GAAP metrics.

PROJECTS UPDATE10

Newmont’s project pipeline supports stable production with improving margins and mine life. Newmont’s 2022 and longer-term outlook includes current development capital costs and production related to Tanami Expansion 2, Ahafo North, Yanacocha Sulfides, Pamour and Cerro Negro District Expansion 1. Additional projects not listed below represent incremental improvements to the Company’s outlook.

- Tanami Expansion 2 (Australia) secures Tanami’s future as a long-life, low-cost producer to extend mine life beyond 2040 through the addition of a 1,460 meter hoisting shaft and supporting infrastructure to process 3.3 million tonnes per year and provide a platform for future growth. The expansion is expected to increase average annual gold production by approximately 150,000 to 200,000 ounces per year for the first five years and reduce operating costs by approximately 10 percent. Development costs (excluding capitalized interest) since approval were $395 million, of which $111 million related to the six months ended June 30, 2022. Total capital costs are expected to be approximately 25% above the prior estimate, incorporating the significant impacts from Covid-related restrictions and protocols and the current market conditions for labor and materials. Commercial production for the project is now expected to be in early 2025. Formal updates to capital estimates and estimated project completion will be provided later in the year.

- Ahafo North (Africa) expands our existing footprint in Ghana with four open pit mines and a stand-alone mill located approximately 30 kilometers from the Company’s Ahafo South operations. The project is expected to add between 275,000 and 325,000 ounces per year for the first five full years of production. Ahafo North is the best unmined gold deposit in West Africa with approximately 3.5 million ounces of Reserves and more than 1 million ounces of Measured, Indicated and Inferred Resources and significant upside potential to extend beyond Ahafo North’s current 13-year mine life. Development costs (excluding capitalized interest) since approval were $142 million, of which $75 million related to the six months ended June 30, 2022. Total capital costs are expected to be approximately 15% above the prior estimate, incorporating the cost associated with delayed land access. Commercial production for the project is now expected to be in mid-2025. Formal updates to capital estimates and estimated project completion will be provided later in the year.

- Yanacocha Sulfides (South America) will develop the first phase of sulfide deposits and an integrated processing circuit, including an autoclave to produce 45% gold, 45% copper and 10% silver. The project is expected to add average annual production of 525,000 gold equivalent ounces per year for the first five full years (2027-2031). Total capital costs for the project are estimated at $2.5 billion from the investment decision date, expected in late 2022, with a three year development period. The first phase focuses on developing the Yanacocha Verde and Chaquicocha deposits to extend Yanacocha’s operations beyond 2040 with second and third phases having the potential to extend life for multiple decades.

- Pamour (North America) extends the life of Porcupine and maintains production beginning in 2024. The project will optimize mill capacity, adding volume and supporting high grade ore from Borden and Hoyle Pond, while supporting further exploration in a highly prospective and proven mining district. An investment decision is expected in the second half of 2022 with estimated capital costs between $350 and $450 million.

- Cerro Negro District Expansion 1 (South America) includes the simultaneous development of the Marianas and Eastern districts to extend the mine life of Cerro Negro beyond 2030. The project is expected to improve production to above 350,000 ounces beginning in 2024. Development capital costs for the project are estimated to be approximately $300 million. This project provides a platform for further exploration and future growth through additional expansions.

- Attributable gold production for the second quarter 2022 includes 70 thousand ounces from the Company’s equity method investment in Pueblo Viejo (40%).

- Non-GAAP measure. See end of this release for reconciliation to Costs applicable to sales.

- Non-GAAP measure. See end of this release for reconciliation to Costs applicable to sales.

- Non-GAAP measure. See end of this release for reconciliation to Net income (loss) attributable to Newmont stockholders.

- Non-GAAP measure. See end of this release for reconciliation to Net income (loss) attributable to Newmont stockholders.

- Capital expenditures refers to Additions to property plant and mine development from the Condensed Consolidated Statements of Cash Flows.

- Non-GAAP measure. See end of this release for reconciliation to Net cash provided by operating activities.

- Non-GAAP measure. See end of this release for reconciliation.

- Non-GAAP measure. See end of this release for reconciliation.

- Project estimates remain subject to change based upon uncertainties, including future impacts of Covid-19 and other cost pressures, supply chain disruptions and availabilities, commodity price volatility and other factors, which may impact estimated capital expenditures, AISC and timing of projects. See end of this release for cautionary statement regarding forward-looking statements.

UPDATED OUTLOOK

Newmont is providing updated 2022 outlook due to impacts on gold production estimates in the first half of the year, as well as the continued impact from inflationary pressures on costs. Please see the cautionary statement in the end notes for additional information. For further discussion, investors are encouraged to attend Newmont’s Second Quarter 2022 Earnings Conference Call.

Newmont’s updated 2022 outlook includes 6.0 million ounces of attributable gold production and 1.3 million gold equivalent ounces from copper, silver, lead and zinc. The revised outlook for attributable gold production includes negative impacts from operational challenges at Ahafo, a transition to a leach-only operation at CC&V, as well as challenges from a competitive labor market, primarily in Canada and Australia.

Ahafo experienced challenges due to labor availability and supply chain disruptions impacting the delivery of new equipment and critical spares, which affected our ability to ramp-up mining rates at Subika Underground. As a result, Ahafo’s full-year production was reduced by approximately 80 thousand ounces. The CC&V operation has begun the transition to a higher-value, longer-life leach-only operation, resulting in a reduction in full-year production of approximately 40 thousand ounces. In addition, Newmont continues to experience lower productivity as a result of a competitive labor market in Canada in Australia, resulting in full-year production impacts of approximately 50 thousand ounces and 30 thousand ounces in those regions, respectively.

Updated 2022 CAS outlook is expected to be $900 per gold ounce and $750 per co-product gold equivalent ounce. Updated 2022 AISC outlook is expected to be $1,150 per gold ounce and $1,050 per co-product gold equivalent ounce. The revised outlook includes the impact from lower production volumes and higher direct operating costs related to labor, energy, consumables and supplies as a result of sustained inflationary pressures.

Development capital is expected to be $1.1 billion for 2022 to incorporate delays in spending at Yanacocha Sulfides and Ahafo North.

General and administrative expense is expected to be $270 million, incorporating slight increases in labor costs due to inflationary pressures. Interest expense is expected to be $200 million, a reduction of $25 million following the timely refinancing of our 2022 and 2023 notes in December of last year.

| Newmont 2022 Outlook a | Updated (as of July 25, 2022) | Previous (as of Dec. 2, 2021) |

| Consolidated Gold Production (Moz) | 5.9 | 6.1 |

| Attributable Gold Production (Moz) b | 6.0 | 6.2 |

| Consolidated Gold CAS ($/oz) | 900 | 820 |

| Consolidated Gold AISC($/oz) c | 1,150 | 1,050 |

| Consolidated Co-Product GEO Production (Moz) d | 1.3 | 1.3 |

| Attributable Co-Product GEO Production (Moz) d | 1.3 | 1.3 |

| Consolidated Co-Product GEO CAS ($/oz) d | 750 | 675 |

| Consolidated Co-Product GEO AISC ($/oz) c,d | 1,050 | 975 |

| Consolidated Total GEO Production (Moz) d | 7.2 | 7.4 |

| Attributable Total GEO Production (Moz) d | 7.3 | 7.5 |

| Consolidated Total GEO CAS ($/oz) d | 875 | 800 |

| Consolidated Total GEO AISC ($/oz) c,d | 1,130 | 1,030 |

| Consolidated Sustaining Capital Expenditures ($M) | 1,000 | 1,000 |

| Consolidated Development Capital Expenditures ($M) | 1,100 | 1,400 |

| Attributable Sustaining Capital Expenditures ($M) | 925 | 925 |

| Attributable Development Capital Expenditures ($M) e | 1,100 | 1,400 |

| General & Administrative ($M) | 270 | 260 |

| Interest Expense ($M) | 200 | 225 |

| Depreciation and Amortization ($M) | 2,300 | 2,300 |

| Exploration & Advanced Projects ($M) | 450 | 450 |

| Adjusted Tax Rate f,g | 30% – 34% | 30% – 34% |

a. 2022 outlook projections are considered forward-looking statements and represent management’s good faith estimates or expectations of future production results as of July 25, 2022. Outlook is based upon certain assumptions, including, but not limited to, metal prices, oil prices, certain exchange rates and other assumptions. For example, updated 2022 Outlook includes actual results through June 30, 2022 and assumes $1,800/oz Au, $4.10/lb Cu, $21.00/oz Ag, $1.60/lb Zn, $0.95/lb Pb, $0.74 USD/AUD exchange rate, $0.80 USD/CAD exchange rate and $110/barrel WTI for the second half of 2022. Production, CAS, AISC and capital estimates exclude projects that have not yet been approved, except for Yanacocha Sulfides, Pamour and Cerro Negro District Expansion 1 which are included in Outlook. The potential impact on inventory valuation as a result of lower prices, input costs, and project decisions are not included as part of this Outlook. Assumptions used for purposes of Outlook may prove to be incorrect and actual results may differ from those anticipated, including variation beyond a +/-5% range. Outlook cannot be guaranteed. As such, investors are cautioned not to place undue reliance upon Outlook and forward-looking statements as there can be no assurance that the plans, assumptions or expectations upon which they are placed will occur. Amounts may not recalculate to totals due to rounding. See cautionary at the end of this release.

b. Attributable gold production outlook includes the Company’s equity investment (40%) in Pueblo Viejo with ~285Koz in 2022; does not include the Company’s other equity investments. Attributable gold production outlook represents the Company’s 75% interest in Merian.

c. All-in sustaining costs (AISC) as used in the Company’s Outlook is a non-GAAP metric; see below for further information and reconciliation to consolidated 2022 CAS outlook.

d. Gold equivalent ounces (GEO) is calculated as pounds or ounces produced multiplied by the ratio of the other metal’s price to the gold price, using Gold ($1,200/oz.), Copper ($3.25/lb.), Silver ($23.00/oz.), Lead ($0.95/lb.), and Zinc ($1.15/lb.) pricing.

e. Attributable development capital accounts for the acquisition of the remaining interest in Yanacocha, including Buenaventura’s 43.65% interest and Sumitomo Corporation’s 5% interest, as announced on February 8, 2022 and April 12, 2022, respectively.

f. The adjusted tax rate excludes certain items such as tax valuation allowance adjustments.

g. Assuming average prices of $1,800 per ounce for gold, $3.25 per pound for copper, $23.00 per ounce for silver, $0.95 per pound for lead, and $1.15 per pound for zinc and achievement of current production and sales volumes and cost estimates, we estimate our consolidated adjusted effective tax rate related to continuing operations for 2022 will be between 30%-34%.

A conference call will be held on Monday, July 25, 2022 at 10:00 a.m. Eastern Time (8:00 a.m. Mountain Time); it will also be carried on the Company’s website.

Conference Call Details

| Dial-In Number | 844.200.6205 | |

| Intl. Dial-In Number | 929.526.1599 | |

| Dial-In Access Code | 408771 | |

| Conference Name | Newmont | |

| Replay Number | 866.813.9403 | |

| Intl. Replay Number | 44.204.525.0658 | |

| Replay Access Code | 870232 |

Webcast Details

Title: Newmont Second Quarter 2022 Earnings Conference Call

URL: https://events.q4inc.com/attendee/715196742

The second quarter 2022 results will be available before the market opens on Monday, July 25, 2022, on the “Investor Relations” section of the Company’s website, www.newmont.com. Additionally, the conference call will be archived for a limited time on the Company’s website.

About Newmont

Newmont is the world’s leading gold company and a producer of copper, silver, zinc and lead. The Company’s world-class portfolio of assets, prospects and talent is anchored in favorable mining jurisdictions in North America, South America, Australia and Africa. Newmont is the only gold producer listed in the S&P 500 Index and is widely recognized for its principled environmental, social and governance practices. The Company is an industry leader in value creation, supported by robust safety standards, superior execution and technical expertise. Newmont was founded in 1921 and has been publicly traded since 1925.

Cautionary Statement Regarding Forward Looking Statements, Including Outlook:

This news release contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are intended to be covered by the safe harbor created by such sections and other applicable laws. Where a forward-looking statement expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, such statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by the forward-looking statements. Forward-looking statements often address our expected future business and financial performance and financial condition; and often contain words such as “anticipate,” “intend,” “plan,” “will,” “would,” “estimate,” “expect,” “believe,” or “potential.” Forward-looking statements in this news release may include, without limitation, (i) estimates of future production and sales, including production outlook, average future production and upside potential; (ii) estimates of future costs applicable to sales and all-in sustaining costs; (iii) estimates of future capital expenditures, including development and sustaining capital; (iv) expectations regarding the Tanami Expansion 2, Ahafo North, Yanacocha Sulfides, Pamour and Cerro Negro District Expansion 1 projects, including, without limitation, expectations for production, milling, costs applicable to sales and all-in sustaining costs, capital costs, mine life extension, construction completion, commercial production and other timelines; (v) expectations regarding future investments or divestitures; (vi) expectations regarding free cash flow and returns to stockholders, including with respect to future dividends and future share repurchases; and (vii) other outlook. Estimates or expectations of future events or results are based upon certain assumptions, which may prove to be incorrect. Such assumptions, include, but are not limited to: (i) there being no significant change to current geotechnical, metallurgical, hydrological and other physical conditions; (ii) permitting, development, operations and expansion of operations and projects being consistent with current expectations and mine plans; (iii) political developments in any jurisdiction in which the Company operates being consistent with its current expectations; (iv) certain exchange rate assumptions; (v) certain price assumptions for gold, copper, silver, zinc, lead and oil; (vi) prices for key supplies; (vii) the accuracy of current mineral reserve and mineralized material estimates; and (viii) other planning assumptions. Uncertainties relating to the impacts of Covid-19, include, without limitation, general macroeconomic uncertainty and changing market conditions, changing restrictions on the mining industry in the jurisdictions in which we operate, the ability to operate following changing governmental restrictions on travel and operations (including, without limitation, the duration of restrictions, including access to sites, ability to transport and ship doré, access to processing and refinery facilities, impacts to international trade, impacts to supply chain, including price, availability of goods, ability to receive supplies and fuel, impacts to productivity and operations in connection with decisions intended to protect the health and safety of the workforce, their families and neighboring communities), the impact of additional waves or variations of Covid, and the availability and impact of Covid vaccinations in the areas and countries in which we operate. Such uncertainties could result in operating sites being placed into care and maintenance and impact estimates, costs and timing of projects. Although the Company does not currently have operations in Ukraine, Russia or other parts of Europe, Russia’s invasion of Ukraine has resulted in uncertainties in the market which could impact certain planning assumptions, including, but not limited to commodity and currency prices, costs and supply chain availabilities. Investors are reminded that future dividends beyond the dividend payable on September 22, 2022 to holders of record at the close of business on September 8, 2022 have not yet been approved or declared by the Board of Directors, and an annualized dividend payout or dividend yield has not been declared by the Board. Management’s expectations with respect to future dividends are “forward-looking statements” and the Company’s dividend framework is non-binding. The declaration and payment of future dividends remain at the discretion of the Board of Directors and will be determined based on Newmont’s financial results, balance sheet strength, cash and liquidity requirements, future prospects, gold and commodity prices, and other factors deemed relevant by the Board. Investors are also cautioned that the extent to which the Company repurchases its shares, and the timing of such repurchases, will depend upon a variety of factors, including trading volume, market conditions, legal requirements, business conditions and other factors. The repurchase program may be discontinued at any time, and the program does not obligate the Company to acquire any specific number of shares of its common stock or to repurchase the full authorized amount during the authorization period. Consequently, the Board of Directors may revise or terminate such share repurchase authorization in the future. For a more detailed discussion of risks and other factors that might impact future looking statements, see the Company’s Annual Report on Form 10-K for the year ended December 31, 2021 and the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2022, each filed with the U.S. Securities and Exchange Commission (the “SEC”), under the heading “Risk Factors”, available on the SEC website or www.newmont.com. The Company does not undertake any obligation to release publicly revisions to any “forward-looking statement,” including, without limitation, outlook, to reflect events or circumstances after the date of this news release, or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws. Investors should not assume that any lack of update to a previously issued “forward-looking statement” constitutes a reaffirmation of that statement. Continued reliance on “forward-looking statements” is at investors’ own risk.

Notice Regarding Reserve and Resource:

Unless otherwise stated herein, the reserves stated in this release represent estimates at December 31, 2021, which could be economically and legally extracted or produced at the time of the reserve determination. Estimates of proven and probable reserves are subject to considerable uncertainty. Such estimates are, or will be, to a large extent, based on metal prices and interpretations of geologic data obtained from drill holes and other exploration techniques, which data may not necessarily be indicative of future results. Additionally, resource does not indicate proven and probable reserves as defined by the SEC or the Company’s standards. Estimates of measured, indicated and inferred resource are subject to further exploration and development, and are, therefore, subject to considerable uncertainty. Inferred resources, in particular, have a great amount of uncertainty as to their existence and their economic and legal feasibility. The Company cannot be certain that any part or parts of the resource will ever be converted into reserves. For additional information on our reserves and resources, please see Item 2 of the Company’s Form 10-K, filed on February 24, 2022 with the SEC.

Media Contact

Courtney Boone 303.837.5159 [email protected]

Investor Contact

Daniel Horton 303.837.5468 [email protected]

Source: Newmont Corporation

Original Article: https://www.newmont.com/investors/news-release/news-details/2022/Newmont-Announces-Second-Quarter-2022-Results/default.aspx